One of the first things people run into when trying to pay off debt is the internet immediately demanding they pick a side.

Debt snowball.

Debt avalanche.

Math versus motivation.

Spreadsheet logic versus emotional momentum.

Personal finance discussions love treating this like a dramatic philosophical battle when, realistically, most people are just trying to survive adulthood without developing a stress twitch every time they open their banking app.

The truth is that both methods can work. The better question is usually:

“Which strategy are you actually likely to stick with long enough to make progress?”

Symptom

“I want to pay off debt, but I don’t know where to start.”

Common side effects may include:

- staring at multiple balances and doing nothing

- paying random amounts toward random debts

- switching strategies every two weeks after watching finance videos at midnight

- feeling overwhelmed before the plan even starts

A payoff strategy matters because decision fatigue alone can slow people down.

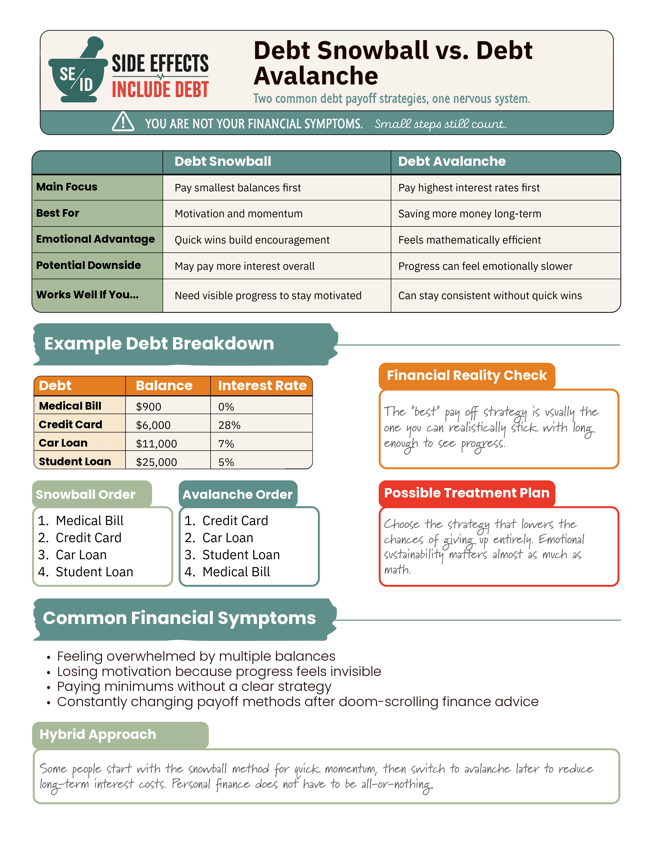

What Is the Debt Snowball Method?

The debt snowball method focuses on paying off the smallest balances first, regardless of interest rate.

You continue making minimum payments on all debts, but throw extra money toward the smallest balance until it’s eliminated. Then you roll that payment into the next-smallest debt.

The idea is that small wins create momentum.

Example Snowball Order

| Debt | Balance | Interest Rate |

|---|---|---|

| Medical Bill | $900 | 0% |

| Credit Card | $6,000 | 28% |

| Car Loan | $11,000 | 7% |

| Student Loan | $25,000 | 5% |

Under the snowball method, the payoff order would be:

- Medical Bill

- Credit Card

- Car Loan

- Student Loan

Even though the medical bill has no interest, paying it off first creates a quick psychological win.

The debt snowball method is designed around motivation and visible progress, not pure mathematical optimization.

What Is the Debt Avalanche Method?

The debt avalanche method focuses on paying off the highest interest rates first.

Instead of prioritizing small balances, you attack the debt causing the most financial damage over time.

Using the same example above, avalanche order would look like:

- Credit Card

- Car Loan

- Student Loan

- Medical Bill

This method usually saves more money long-term because high-interest balances stop growing as aggressively.

Why People Choose Avalanche

The avalanche method tends to appeal to people who:

- like efficiency

- stay motivated without quick wins

- want to reduce total interest paid

- prefer mathematically optimized systems

But emotionally, avalanche can sometimes feel slower because the balances themselves may take longer to disappear.

The Emotional Side of Debt Payoff

One thing finance advice often ignores is that debt is not purely mathematical.

It’s emotional.

Behavioral.

Psychological.

Two people with identical balances may need completely different payoff systems to stay consistent.

Some people feel energized by:

- knocking out small debts quickly

- seeing fewer accounts

- reducing mental clutter

Others feel more motivated by:

- reducing interest aggressively

- seeing long-term savings

- optimizing payoff efficiency

Neither approach is morally superior.

The best debt payoff method is usually the one that lowers the chances of giving up entirely.

Consistency matters more than perfection.

The Hybrid Approach

A lot of people naturally end up using a hybrid method.

For example:

- paying off one or two small annoying balances first

- then switching to avalanche later

- or prioritizing emotionally stressful debts regardless of balance size

Personal finance does not have to become a strict identity or ideology.

The goal is reducing debt while keeping the system sustainable enough to continue long-term.

Financial Symptoms That May Affect Your Strategy

Certain financial patterns may influence which method works better for you.

Snowball May Help If:

- motivation disappears quickly

- large balances feel emotionally paralyzing

- you need visible progress

- multiple small debts create stress

Avalanche May Help If:

- interest rates are extremely high

- you stay motivated by long-term efficiency

- your debt balances are already large

- minimizing total repayment cost is the priority

Sometimes the “correct” strategy on paper is not the strategy your nervous system can realistically tolerate for five years.

Related Resource

To help compare both payoff methods visually, I created a printable:

Debt Snowball vs Debt Avalanche Comparison Guide.

It includes:

- side-by-side strategy breakdowns

- example debt payoff orders

- emotional vs mathematical comparisons

- hybrid strategy ideas

- common financial symptoms associated with debt overwhelm

Download the Printable Guide:

Final Diagnosis

Debt payoff is rarely just about numbers.

It’s also about:

- emotional sustainability

- stress management

- consistency

- behavior patterns

- and creating a system you can continue even when motivation drops

Because a payoff plan that technically works but completely burns you out halfway through is probably not the long-term solution either.

Leave a comment