For a lot of borrowers, one of the most frustrating parts of student loans is making payments and still watching the balance barely move.

Or worse, watching it grow.

It feels backwards. You pay. The number should go down. That feels like the agreement, right? Instead, you log into your account six months later and somehow owe more than before, which is a very bold choice from a balance that was supposed to be decreasing.

Unfortunately, this is pretty common, especially with federal student loans and income-driven repayment plans. It does not always mean you did something wrong. Sometimes it means your payment plan is working the way it was designed to work, just not in the emotionally satisfying way most people expect.

Making a payment does not always mean your principal balance is shrinking.

Symptom

“My balance keeps growing even though I’m making payments.”

This is one of those student loan problems that feels fake until it happens to you. You make the payment, the money leaves your bank account, and then the loan balance just sits there looking mostly unchanged. Occasionally it even increases, because apparently the numbers wanted to add a little drama.

Some common side effects include avoiding your loan dashboard, feeling like your payment disappears into a void, pretending interest does not exist for emotional stability, and wondering whether the math has personally betrayed you.

This symptom usually shows up when your payment is not large enough to cover the interest that builds each month.

Diagnosis

The main culprit is usually interest accrual.

Student loans collect interest over time. Depending on your interest rate and repayment plan, your monthly payment may not fully cover the interest that builds each month. When that happens, your payment may help, but it may not be enough to reduce the main balance.

Here’s a simple example:

| Loan Detail | Example |

|---|---|

| Loan balance | $47,000 |

| Interest rate | 6% |

| Approximate monthly interest | $235 |

| Monthly IDR payment example | $120 |

| Unpaid interest for the month | About $115 |

In that example, the borrower is making payments, but the payment does not fully cover the monthly interest. That means the loan may not shrink much, and depending on the situation, the balance may continue growing.

That is the part that confuses people. Most of us are used to thinking of debt like a regular installment loan where every payment makes the total smaller. Student loans, especially on income-driven repayment plans, can work differently.

Income-driven repayment plans are often designed around affordability. The goal may be to keep the monthly payment manageable, prevent default, and preserve a path toward forgiveness. The goal is not always fast payoff.

Some repayment plans are designed to lower your monthly payment, not aggressively attack your principal balance.

Why the Balance Can Jump Suddenly

Slow growth is frustrating enough, but sometimes the balance appears to jump all at once. That can happen when unpaid interest gets added to the principal balance, which is called capitalization.

Capitalization can make the balance more expensive because future interest may be calculated on a larger principal amount. Very rude behavior, mathematically speaking.

Some common situations that may affect your balance include:

| Situation | Why It Matters |

|---|---|

| Forbearance | Payments may pause, but interest may still build depending on the loan and program rules. |

| Deferment | Some loans may continue accruing interest during deferment. |

| Repayment plan changes | Switching plans can affect how interest is handled. |

| Consolidation | Combining loans may change the structure of your debt. |

| Missed recertification | Your payment could increase if income information is not updated on time. |

| Returning to school | In-school status may pause payments, but not all loans stop accruing interest. |

Recently, SAVE-related court issues and administrative forbearances have made things even more confusing for borrowers. Some people have been unsure whether their payments are paused, whether interest is accruing, or when repayment will restart.

That uncertainty makes it harder to tell what is normal, what is temporary, and what needs attention.

Behavioral Side Effects

The financial part is only half of the problem. The emotional side matters too.

When your balance barely moves, it can make progress feel invisible. That is when a lot of people stop checking their accounts, avoid opening statements, lose motivation to pay extra, or assume they are failing somehow.

But a growing balance does not automatically mean you are bad with money.

Sometimes it means the system is confusing. Sometimes it means your payment is too low to cover interest. Sometimes it means your repayment plan is prioritizing affordability now over payoff speed later.

And sometimes it means you need better information before deciding what to do next.

Avoiding the balance usually makes the stress louder. Checking it gives you information, not a moral judgment.

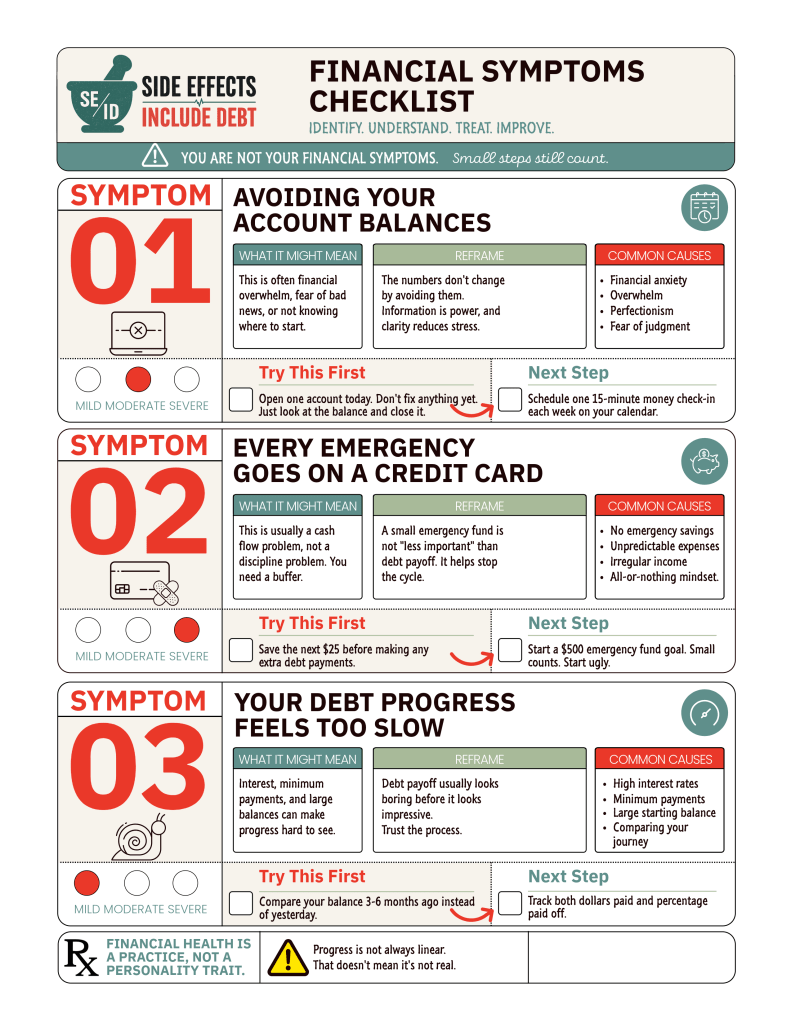

Related Resource: Financial Symptoms Checklist

When student loan balances grow despite making payments, the stress usually goes beyond the numbers. It can show up as avoidance, repayment fatigue, anxiety around account balances, or frustration because progress feels too slow.

I created a printable Financial Symptoms Checklist to help organize those patterns. It includes common financial stress symptoms, possible causes, reframes, and small action steps to help you respond without spiraling.

Because sometimes the first step is not fixing everything. Sometimes it is figuring out what is actually happening and giving yourself a place to start.

Download: Financial Symptoms Checklist

Treatment Plan

The best next step depends on your loan type, income, interest rate, repayment plan, and whether you are working toward forgiveness.

For some borrowers, paying extra toward principal may make sense. For others, staying on an income-driven repayment plan and pursuing forgiveness may be the better long-term strategy. There is not one perfect answer, which is deeply inconvenient but also true.

A few possible treatment options include:

| Option | When It Might Help |

|---|---|

| Review your repayment plan | If your payment does not cover monthly interest or your income has changed. |

| Pay extra toward principal | If you can afford it and want to reduce the balance faster. |

| Pursue forgiveness programs | If you qualify for PSLF or long-term IDR forgiveness. |

| Build emergency savings first | If every surprise expense sends you back into more debt. |

| Refinance private loans | If your loans are private and you can get a better rate. Be careful with federal loans because refinancing can remove federal protections. |

| Prioritize higher-interest debt | If credit cards or other debts are costing you more than your student loans. |

The important thing is to avoid reacting out of panic. A growing balance feels awful, but the solution depends on why it is growing.

If your payment is low because you are on an income-driven repayment plan and pursuing forgiveness, that may be part of the plan. If your payment is low because you did not realize interest was building faster than you were paying, that may call for a different strategy.

Things to Monitor

If your student loan balance keeps growing, start by checking a few key details. You do not have to solve the entire debt situation in one sitting. This is a checkup, not a financial exorcism.

| What to Check | Why It Matters |

|---|---|

| Current repayment plan | Your plan affects payment amount, interest handling, and forgiveness options. |

| Interest rate | Higher interest means the balance can grow faster. |

| Monthly interest amount | Helps you see whether your payment covers interest. |

| Payment amount | A low payment may be manageable but may not reduce principal. |

| Capitalized interest | This can increase the amount future interest is based on. |

| Subsidized vs. unsubsidized loans | Subsidized loans may have different interest benefits in certain periods. |

| Forgiveness eligibility | Your strategy may change if forgiveness is realistic. |

| Servicer notices | Payment restart dates, plan changes, and recertification deadlines matter. |

Final Diagnosis

If your student loan balance grows while you are making payments, it does not automatically mean you are doing something wrong.

It may mean your monthly payment is not covering the interest. It may mean unpaid interest has capitalized. It may mean your repayment plan is designed more for affordability than fast payoff. Or it may mean the loan system is doing what it often does best: making a simple concept unnecessarily difficult to understand.

The goal is not to panic-pay or ignore the balance forever.

The goal is to understand what is happening, decide what strategy actually fits your situation, and stop treating every confusing loan update like a personal failure.

Because sometimes the issue is not simply “pay more.”

Sometimes the first treatment is learning how the system works behind the scenes.

Related Articles to Check Out

If your student loan balance is growing, this article is probably only one piece of the puzzle. These related articles can help you figure out what is happening and what to do next.

| Article | Why It Helps |

|---|---|

| SAVE vs. RAP: Explained in Plain English | Breaks down the repayment plan changes and what borrowers may need to watch as SAVE transitions. |

| Checklist Before Your Student Loan Payment Restarts | Helps you check your loan status, payment amount, interest, servicer notices, and budget before payments resume. |

| Debt Snowball vs. Debt Avalanche: Which Payoff Method Actually Works Better? | Helpful if you are comparing student loans with credit cards, car loans, or other debts. |

| How to Build an Emergency Fund While You’re Still in Debt | Explains why saving a small buffer can sometimes prevent more debt later. |

| “Your Loans Qualify”: How Student Loan Scam Calls Work | Helps you spot warning signs when scammers use repayment confusion to sound official. |

Leave a comment