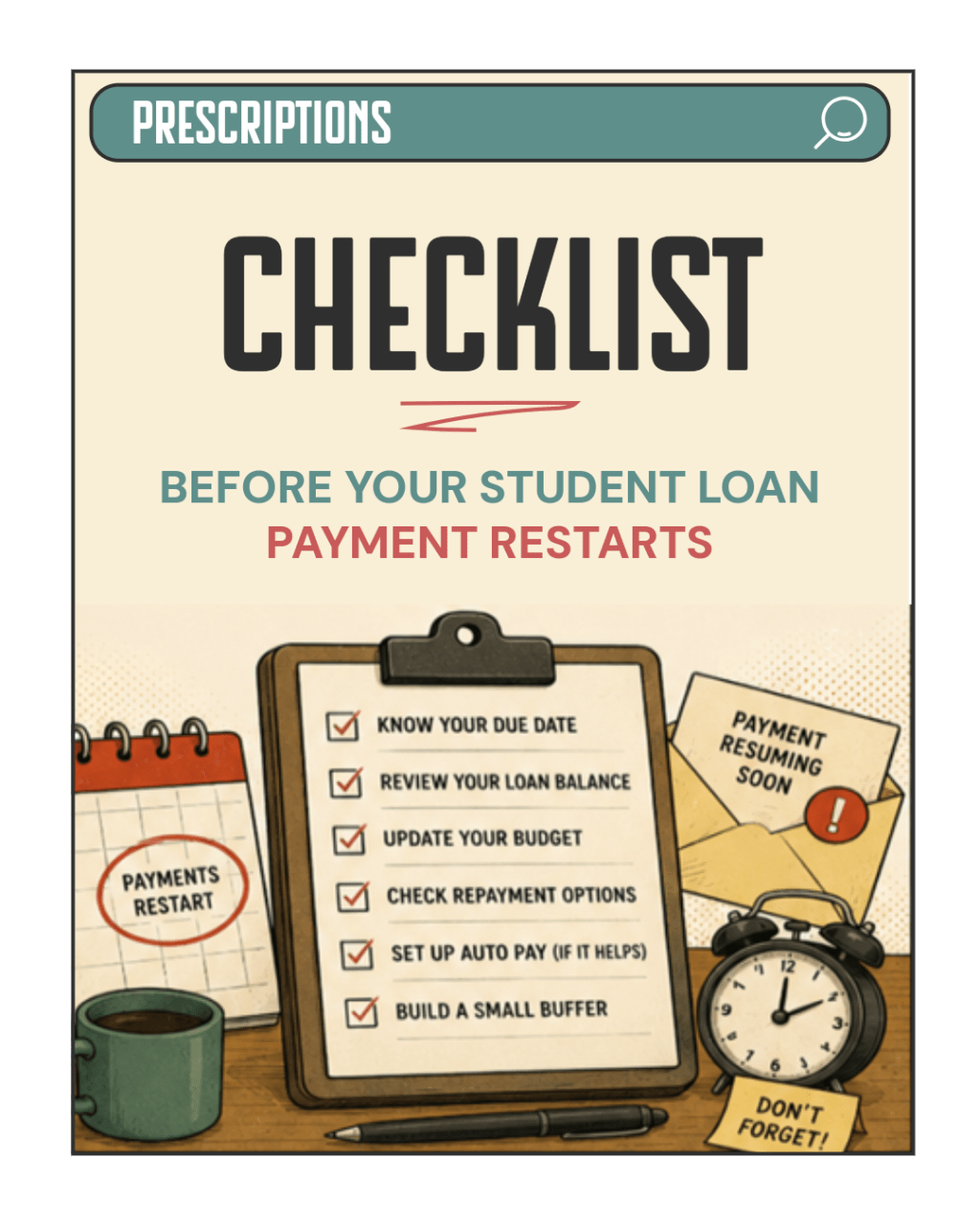

For millions of borrowers, federal student loan repayment restarting has felt less like a scheduled event and more like spotting movement in the woods and hoping it is not another servicer notice.

Between repayment pauses, SAVE-related forbearances, legal challenges, changing guidance, and shifting repayment plans, a lot of people genuinely do not know whether they currently owe a payment, when that payment starts, how much it will be, or whether interest is building right now. Your original checklist already hits those main points, so this version keeps the same bones while making it fit the newer article format.

If your loans are about to re-enter repayment, this is the pre-payment checkup to do before the first payment hits your account like an uninvited guest with a clipboard.

The goal is not to become a student loan expert overnight. The goal is to know what system you are standing inside before money starts moving again.

Symptom

“I just got a notice saying my payment is restarting, and I have absolutely no idea what is happening.”

This is a very normal reaction right now. A lot of borrowers have been moved through pauses, forbearances, plan changes, servicer updates, and repayment notices that are not exactly written in calming bedtime-story language.

Common side effects may include panic-logging into your servicer portal, discovering your password expired sometime during the Bronze Age, staring at the phrase “administrative forbearance” like it is a curse from an old library book, and checking Reddit before checking your actual account.

The problem is not just that payments are restarting. The problem is that many borrowers are trying to restart repayment without a clear understanding of their current loan status, payment plan, due date, interest situation, or next steps.

Diagnosis

Student loan repayment does not always restart in a clean, obvious way.

Your loans may be in repayment, deferment, forbearance, processing status, delinquency, or some other account condition that sounds simple until you try to figure out what it means for your actual bank account.

Before you make any big decision, start with the basics:

| What to Check | Why It Matters |

|---|---|

| Current loan status | Tells you whether your loans are actually in repayment or still paused. |

| Payment due date | Helps you avoid missing the first payment by accident. |

| Monthly payment amount | Lets you plan your budget before the draft hits. |

| Current repayment plan | Determines how your payment is calculated. |

| Interest status | Helps you understand whether your balance may be growing. |

| Servicer notices | May include deadlines, plan changes, or action steps. |

A lot of repayment panic comes from not knowing which of these details changed. And to be fair, the system has not exactly been sending handwritten thank-you notes with clear bullet points and emotional support snacks.

Treatment Plan

Confirm Your Current Loan Status

Start by logging directly into your student loan servicer account. Not through a random email link. Not through a text message. Not through a mysterious “loan relief” company that sounds like it was named by a committee of suspicious robots.

Go straight to your official servicer website and check your current status.

Your loans might show as active repayment, administrative forbearance, deferment, delinquent, awaiting recertification, or processing under an IDR application. The exact wording matters because each status can affect whether you owe a payment now, whether interest is building, and whether you need to take action.

Do not assume your loans are still paused just because they were paused before.

Verify Your Repayment Plan

Once you know your loan status, check your repayment plan.

Many borrowers who were on SAVE, applied for SAVE, or were placed into SAVE-related forbearance may need to pay extra attention to account updates. Some borrowers may eventually need to recertify income, choose another repayment option, or review their payment amount.

This is not the place to rely on memory. Your account may not be in the plan you think it is.

| Question | What You’re Looking For |

|---|---|

| What plan am I currently listed under? | Standard, IDR, SAVE-related status, forbearance, or something else. |

| Was my IDR application processed? | Pending applications can affect payment timing. |

| Is my income information current? | Old income data may change estimated payments. |

| Did my payment amount change? | Even a small change can affect your monthly budget. |

The deeply irritating truth is that repayment plans are not always “set it and forget it.” Sometimes they are “set it, forget it, receive a confusing notice, and then spend 40 minutes hunting for the place where the website hid the important information.”

Update Your Contact Information

This step sounds too basic to matter, which is exactly why it matters.

If your email address, mailing address, phone number, or autopay information is outdated, you may miss notices that actually affect your repayment. And unfortunately, “I never saw it” does not always stop a payment from becoming due.

Take a few minutes to check:

| Contact Item | Status |

|---|---|

| Email address | Current / Needs update |

| Mailing address | Current / Needs update |

| Phone number | Current / Needs update |

| Autopay account | Current / Needs update |

| Notification settings | Current / Needs update |

This is not glamorous financial work. It is the equivalent of checking the batteries in the smoke detector. Boring, but you will be very glad you did it before something starts beeping.

Check Whether Interest Is Accruing

One of the most confusing parts of repayment changes is figuring out whether interest is currently building.

Interest can depend on your loan type, repayment plan, forbearance or deferment status, administrative processing, and recent policy changes. That means two borrowers may be in similar-looking situations but have different interest outcomes.

Look for signs like a growing balance, daily interest listed in your account, unpaid interest, or capitalization notices.

This is especially important if your payment is lower than the amount of interest that builds each month. In that situation, you may be making payments without seeing much movement in the balance, which feels personally offensive but is often just how the math works.

If your payment does not cover the interest, your balance may not decrease the way you expect.

Review Your Budget Before the Payment Hits

A lot of borrowers got used to not having federal student loan payments in their monthly budget. Even if the new payment is not huge, it can still affect groceries, credit card payments, savings, gas, emergency funds, subscriptions, and cash flow timing.

Before repayment restarts, look at the month ahead instead of pretending future-you will solve it with vibes and leftover paycheck crumbs.

Ask yourself:

| Budget Question | Why It Matters |

|---|---|

| When is the payment due? | Timing can matter as much as the amount. |

| Will autopay draft before or after payday? | Prevents accidental overdraft stress. |

| What category will shrink? | Groceries, savings, extra debt payments, etc. |

| Do I need to pause extra payments elsewhere? | Required payments should come before bonus payoff goals. |

| Do I have any emergency cushion? | Even a small buffer can reduce panic. |

Preventative care is easier than financial triage. It is much better to adjust the budget now than to discover the payment hit three days before payday and immediately start negotiating with your checking account.

Decide on a Strategy Before You Panic

Not every borrower should handle repayment the same way.

Some people may want to pay aggressively. Some may be working toward forgiveness. Some may need the lowest manageable payment while they stabilize other parts of their financial life. Some may need to focus on high-interest credit card debt before throwing extra money at lower-interest student loans.

The right strategy depends on income, loan balance, interest rates, job stability, forgiveness eligibility, and overall financial health.

Here are a few possible approaches:

| Strategy | When It Might Make Sense |

|---|---|

| Minimum payment strategy | You need cash flow room or are pursuing forgiveness. |

| Aggressive payoff | You can afford extra payments and want the debt gone faster. |

| Forgiveness path | You qualify for PSLF or long-term IDR forgiveness. |

| Emergency fund first | You keep relying on credit cards for surprise expenses. |

| High-interest debt first | Credit cards or other debts are costing more than student loans. |

| Temporary stabilization | Your budget needs a calm month before big payoff decisions. |

The main thing is to avoid making a rushed decision while emotionally cornered by a repayment notice. Panic is not a financial strategy. It is a smoke alarm with shoes.

Save Documentation

This part is boring, but it can save you later.

Keep copies of repayment notices, plan approvals, IDR applications, payment confirmations, servicer messages, and screenshots of balances or account statuses.

Student loan systems sometimes behave like a group project where nobody remembers who edited the final document. Having your own records gives you something to refer back to if your payment amount changes, your status looks wrong, or your servicer gives conflicting information.

Documentation is not exciting. It is just future-you leaving a trail of breadcrumbs through the policy forest.

Things to Monitor

Once repayment is restarting, you do not have to check your account every hour like it is a flight delay board. But you should monitor the details that could affect your payment or balance.

| Monitor This | Why It Matters |

|---|---|

| Repayment status | Confirms whether payment is actually due. |

| Payment amount | Helps you catch unexpected changes. |

| Interest accrual | Explains why your balance may move. |

| Recertification deadlines | Missing one can affect your payment. |

| Servicer notices | May include deadlines or plan changes. |

| SAVE/RAP updates | Repayment rules may keep shifting. |

| Forgiveness eligibility | Your strategy may depend on it. |

| Autopay enrollment | Prevents missed or unexpected payments. |

A monthly check-in is probably enough for most people unless something is actively changing. Put it on your calendar, make it boring, and do not let your loan portal become a haunted house you only enter during emergencies.

Final Diagnosis

Right now, many borrowers are not struggling because they are irresponsible.

They are struggling because the repayment system has changed repeatedly in a short period of time, often with overlapping pauses, lawsuits, servicer transitions, unclear notices, and payment plan changes.

The goal is not perfection.

The goal is to understand your current loan status, know when money is due, check whether interest is building, and make a plan before the payment restarts.

Because the first student loan payment after a long pause should not feel like a jump scare with compound interest.

Related Articles to Check Out

| Article | Why It Helps |

|---|---|

| Navigating Payments: When Student Loans Don’t Decrease | Explains why payments do not always reduce your balance. |

| SAVE vs. RAP Explained in Plain English | Helps make sense of repayment plan changes and transition confusion. |

| What Is IDR and How Does It Actually Work? | Breaks down income-driven repayment in more normal human language. |

| “Your Loans Qualify”: How Student Loan Scam Calls Work | Helps you spot scam calls that take advantage of repayment confusion. |

| Debt Snowball vs. Debt Avalanche | Useful if you are deciding where student loans fit into your larger debt payoff plan. |

| How to Build an Emergency Fund While You’re Still in Debt | Explains why a small buffer can protect you during repayment changes. |

Leave a comment